Reader

Get LLM-friendly input from a URL or a web search. Improve the factuality of your agent, RAG, GenAI system with a simple prefix.

What is Reader?

Feeding web information into LLMs is an important step of grounding, yet it can be challenging. The simplest method is to scrape the webpage and feed the raw HTML. However, scraping can be complex and often blocked, and raw HTML is cluttered with extraneous elements like markups and scripts. The Reader API addresses these issues by extracting the core content from a URL and converting it into clean, LLM-friendly text, ensuring high-quality input for your agent and RAG systems.

Reader for search grounding

LLMs have a knowledge cut-off, meaning they can't access the latest world knowledge. This leads to problems such as misinformation, outdated responses, hallucinations, and other factuality issues. Grounding is absolutely essential for GenAI applications. Reader allows you to ground your LLM with the latest information from the web. Simply prepend

https://s.jina.ai/ to your query, and Reader will search the web and return the top five results with their URLs and contents, each in clean, LLM-friendly text. This way, you can always keep your LLM up-to-date, improve its factuality, and reduce hallucinations.Reader also reads images!

Images on the webpage are automatically captioned using a vision language model in the reader and formatted as image alt tags in the output. This gives your downstream LLM just enough hints to incorporate those images into its reasoning and summarizing processes. This means you can ask questions about the images, select specific ones, or even forward their URLs to a more powerful VLM for deeper analysis!

The best part? It's free!

Reader API is available for free and offers flexible rate limit and pricing. Built on a scalable infrastructure, it offers high accessibility, concurrency, and reliability. We strive to be your preferred grounding solution for your LLMs.

| Endpoint | Description | Rate limit w/o API key | Rate limit with API key | Token counting scheme | Average latency |

|---|---|---|---|---|---|

r.jina.ai | Read a URL return its content, useful for check grounding | 20 RPM | 200 RPM | Based on the output tokens | 3 seconds |

s.jina.ai | Search on the web return top-5 results, useful for search grounding | 5 RPM | 40 RPM | Based on the output tokens for all 5 search results | 10 seconds |

Don't panic! Every new API key contains one million free tokens!

Try the demo

See how Reader searches the web

Raw HTML

Failed to fetch

Reader Output

Title: Dot-com bubble

URL Source: https://en.wikipedia.org/wiki/Dot-com_bubble

Published Time: 2001-12-27T20:26:47Z

Markdown Content:

[](https://en.wikipedia.org/wiki/File:Nasdaq_Composite_dot-com_bubble.svg)

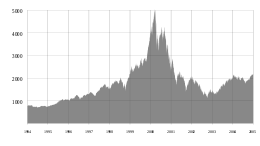

The [NASDAQ Composite](https://en.wikipedia.org/wiki/NASDAQ_Composite "NASDAQ Composite") index spiked in 2000 and then fell sharply as a result of the dot-com bubble.

[](https://en.wikipedia.org/wiki/File:US_VC_funding.png)

Quarterly U.S. venture capital investments, 1995–2017

The **dot-com bubble** (or **dot-com boom**) was a [stock market bubble](https://en.wikipedia.org/wiki/Stock_market_bubble "Stock market bubble") that ballooned during the late-1990s and peaked on Friday, March 10, 2000. This period of market growth coincided with the widespread adoption of the [World Wide Web](https://en.wikipedia.org/wiki/World_Wide_Web "World Wide Web") and the [Internet](https://en.wikipedia.org/wiki/Internet "Internet"), resulting in a dispensation of available [venture capital](https://en.wikipedia.org/wiki/Venture_capital "Venture capital") and the rapid growth of valuations in new dot-com [startups](https://en.wikipedia.org/wiki/Startup_company "Startup company").

Between 1995 and its peak in March 2000, investments in the NASDAQ composite stock market index rose by 800%, only to fall to 78% from its peak by October 2002, giving up all its gains during the bubble.

During the **dot-com crash**, many [online shopping](https://en.wikipedia.org/wiki/Online_shopping "Online shopping") companies, notably [Pets.com](https://en.wikipedia.org/wiki/Pets.com "Pets.com"), [Webvan](https://en.wikipedia.org/wiki/Webvan "Webvan"), and [Boo.com](https://en.wikipedia.org/wiki/Boo.com "Boo.com"), as well as several communication companies, such as [Worldcom](https://en.wikipedia.org/wiki/Worldcom "Worldcom"), [NorthPoint Communications](https://en.wikipedia.org/wiki/NorthPoint_Communications "NorthPoint Communications"), and [Global Crossing](https://en.wikipedia.org/wiki/Global_Crossing "Global Crossing"), failed and shut down.[\[1\]](#cite_note-1)[\[2\]](#cite_note-valuation-2) Others, like [Lastminute.com](https://en.wikipedia.org/wiki/Lastminute.com "Lastminute.com"), [MP3.com](https://en.wikipedia.org/wiki/MP3.com "MP3.com") and [PeopleSound](https://en.wikipedia.org/wiki/PeopleSound "PeopleSound") remained through its sale and buyers acquisition. Larger companies like [Amazon](https://en.wikipedia.org/wiki/Amazon_\(company\) "Amazon (company)") and [Cisco Systems](https://en.wikipedia.org/wiki/Cisco_Systems "Cisco Systems") lost large portions of their market capitalization, with Cisco losing 80% of its stock value.[\[2\]](#cite_note-valuation-2)[\[3\]](#cite_note-3)

Background\[[edit](https://en.wikipedia.org/w/index.php?title=Dot-com_bubble&action=edit§ion=1 "Edit section: Background")\]

--------------------------------------------------------------------------------------------------------------------------------

Historically, the dot-com boom can be seen as similar to a number of other technology-inspired booms of the past, including [railroads](https://en.wikipedia.org/wiki/Railway_mania "Railway mania") in the 1840s, automobiles in the early 20th century, [radio](https://en.wikipedia.org/wiki/Radio "Radio") in the 1920s, [television](https://en.wikipedia.org/wiki/Television "Television") in the 1940s, [transistor](https://en.wikipedia.org/wiki/Transistor "Transistor") electronics in the 1950s, computer time-sharing in the 1960s, and [home computers](https://en.wikipedia.org/wiki/Home_computer "Home computer") and [biotechnology](https://en.wikipedia.org/wiki/Biotechnology "Biotechnology") in the 1980s.[\[4\]](#cite_note-4)

Overview\[[edit](https://en.wikipedia.org/w/index.php?title=Dot-com_bubble&action=edit§ion=2 "Edit section: Overview")\]

----------------------------------------------------------------------------------------------------------------------------

Low interest rates in 1998–99 facilitated an increase in start-up companies.

In 2000, the dot-com bubble burst, and many dot-com startups went out of business after burning through their [venture capital](https://en.wikipedia.org/wiki/Venture_capital "Venture capital") and failing to become [profitable](https://en.wikipedia.org/wiki/Profit_\(accounting\) "Profit (accounting)").[\[5\]](#cite_note-5) However, many others, particularly online retailers like [eBay](https://en.wikipedia.org/wiki/EBay "EBay") and [Amazon](https://en.wikipedia.org/wiki/Amazon_\(company\) "Amazon (company)"), blossomed and became highly profitable.[\[6\]](#cite_note-auto1-6)[\[7\]](#cite_note-auto-7) More conventional retailers found online merchandising to be a profitable additional source of revenue. While some online entertainment and news outlets failed when their seed capital ran out, others persisted and eventually became economically self-sufficient. Traditional media outlets (newspaper publishers, broadcasters and cablecasters in particular) also found the Web to be a useful and profitable additional channel for content distribution, and an additional means to generate advertising revenue. The sites that survived and eventually prospered after the bubble burst had two things in common: a sound business plan, and a niche in the marketplace that was, if not unique, particularly well-defined and well-served.

In the aftermath of the dot-com bubble, telecommunications companies had a great deal of overcapacity as many Internet business clients went bust. That, plus ongoing investment in local cell infrastructure kept connectivity charges low, and helped to make high-speed Internet connectivity more affordable.\[_[citation needed](https://en.wikipedia.org/wiki/Wikipedia:Citation_needed "Wikipedia:Citation needed")_\] During this time, a handful of companies found success developing business models that helped make the World Wide Web a more compelling experience. These include airline booking sites, [Google](https://en.wikipedia.org/wiki/Google "Google")'s [search engine](https://en.wikipedia.org/wiki/Search_engine "Search engine") and its profitable approach to keyword-based advertising,[\[8\]](#cite_note-8) as well as [eBay](https://en.wikipedia.org/wiki/EBay "EBay")'s auction site[\[6\]](#cite_note-auto1-6) and [Amazon.com](https://en.wikipedia.org/wiki/Amazon.com "Amazon.com")'s online department store.[\[7\]](#cite_note-auto-7) The low price of reaching millions worldwide, and the possibility of selling to or hearing from those people at the same moment when they were reached, promised to overturn established business dogma in advertising, [mail-order](https://en.wikipedia.org/wiki/Mail-order "Mail-order") sales, [customer relationship management](https://en.wikipedia.org/wiki/Customer_relationship_management "Customer relationship management"), and many more areas. The web was a new [killer app](https://en.wikipedia.org/wiki/Killer_app "Killer app")—it could bring together unrelated buyers and sellers in seamless and low-cost ways. Entrepreneurs around the world developed new business models, and ran to their nearest [venture capitalist](https://en.wikipedia.org/wiki/Venture_capitalist "Venture capitalist").[\[9\]](#cite_note-9) While some of the new entrepreneurs had experience in business and economics, the majority were simply people with ideas, and did not manage the capital influx prudently. Additionally, many dot-com business plans were predicated on the assumption that by using the Internet, they would bypass the distribution channels of existing businesses and therefore not have to compete with them; when the established businesses with strong existing brands developed their own Internet presence, these hopes were shattered, and the newcomers were left attempting to break into markets dominated by larger, more established businesses.[\[10\]](#cite_note-10)

The dot-com bubble burst in March 2000, with the technology heavy [NASDAQ Composite](https://en.wikipedia.org/wiki/NASDAQ "NASDAQ") index peaking at 5,048.62 on March 10[\[11\]](#cite_note-11) (5,132.52 intraday), more than double its value just a year before. By 2001, the bubble's deflation was running full speed. A majority of the dot-coms had ceased trading, after having burnt through their venture capital and IPO capital, often without ever making a profit. But despite this, the Internet continues to grow, driven by commerce, ever greater amounts of online information, knowledge, [social networking](https://en.wikipedia.org/wiki/Social_networking_service "Social networking service") and access by mobile devices.

Prelude to the bubble\[[edit](https://en.wikipedia.org/w/index.php?title=Dot-com_bubble&action=edit§ion=3 "Edit section: Prelude to the bubble")\]

------------------------------------------------------------------------------------------------------------------------------------------------------

The 1993 release of [Mosaic](https://en.wikipedia.org/wiki/Mosaic_\(web_browser\) "Mosaic (web browser)") and subsequent [web browsers](https://en.wikipedia.org/wiki/Web_browser "Web browser") during the following years gave computer users access to the [World Wide Web](https://en.wikipedia.org/wiki/World_Wide_Web "World Wide Web"), popularizing use of the Internet.[\[12\]](#cite_note-12) Internet use increased as a result of the reduction of the "[digital divide](https://en.wikipedia.org/wiki/Digital_divide "Digital divide")" and advances in connectivity, uses of the Internet, and computer education. Between 1990 and 1997, the percentage of households in the United States owning computers increased from 15% to 35% as computer ownership progressed from a luxury to a necessity.[\[13\]](#cite_note-13) This marked the shift to the [Information Age](https://en.wikipedia.org/wiki/Information_Age "Information Age"), an economy based on [information technology](https://en.wikipedia.org/wiki/Information_technology "Information technology"), and many new companies were founded.

At the same time, a decline in interest rates increased the availability of capital.[\[14\]](#cite_note-14) The [Taxpayer Relief Act of 1997](https://en.wikipedia.org/wiki/Taxpayer_Relief_Act_of_1997 "Taxpayer Relief Act of 1997"), which lowered the top marginal [capital gains tax in the United States](https://en.wikipedia.org/wiki/Capital_gains_tax_in_the_United_States "Capital gains tax in the United States"), also made people more willing to make more speculative investments.[\[15\]](#cite_note-15) [Alan Greenspan](https://en.wikipedia.org/wiki/Alan_Greenspan "Alan Greenspan"), then-[Chair of the Federal Reserve](https://en.wikipedia.org/wiki/Chair_of_the_Federal_Reserve "Chair of the Federal Reserve"), allegedly fueled investments in the stock market by putting a positive spin on stock valuations.[\[16\]](#cite_note-enigma-16) The [Telecommunications Act of 1996](https://en.wikipedia.org/wiki/Telecommunications_Act_of_1996 "Telecommunications Act of 1996") was expected to result in many new technologies from which many people wanted to profit.[\[17\]](#cite_note-now-17)

The bubble\[[edit](https://en.wikipedia.org/w/index.php?title=Dot-com_bubble&action=edit§ion=4 "Edit section: The bubble")\]

--------------------------------------------------------------------------------------------------------------------------------

As a result of these factors, many investors were eager to invest, at any valuation, in any [dot-com company](https://en.wikipedia.org/wiki/Dot-com_company "Dot-com company"), especially if it had one of the [Internet-related prefixes](https://en.wikipedia.org/wiki/Internet-related_prefixes "Internet-related prefixes") or a "[.com](https://en.wikipedia.org/wiki/.com ".com")" [suffix](https://en.wikipedia.org/wiki/Suffix "Suffix") in its name. [Venture capital](https://en.wikipedia.org/wiki/Venture_capital "Venture capital") was easy to raise. [Investment banks](https://en.wikipedia.org/wiki/Investment_bank "Investment bank"), which profited significantly from [initial public offerings](https://en.wikipedia.org/wiki/Initial_public_offering "Initial public offering") (IPO), fueled speculation and encouraged investment in technology.[\[18\]](#cite_note-swindle-18) A combination of rapidly increasing stock prices in the [quaternary sector of the economy](https://en.wikipedia.org/wiki/Quaternary_sector_of_the_economy "Quaternary sector of the economy") and confidence that the companies would turn future profits created an environment in which many investors were willing to overlook traditional metrics, such as the [price–earnings ratio](https://en.wikipedia.org/wiki/Price%E2%80%93earnings_ratio "Price–earnings ratio"), and base confidence on technological advancements, leading to a [stock market bubble](https://en.wikipedia.org/wiki/Stock_market_bubble "Stock market bubble").[\[16\]](#cite_note-enigma-16) Between 1995 and 2000, the Nasdaq Composite stock market index rose 400%. It reached a price–earnings ratio of 200, dwarfing the peak price–earnings ratio of 80 for the Japanese [Nikkei 225](https://en.wikipedia.org/wiki/Nikkei_225 "Nikkei 225") during the [Japanese asset price bubble](https://en.wikipedia.org/wiki/Japanese_asset_price_bubble "Japanese asset price bubble") of 1991.[\[16\]](#cite_note-enigma-16) In 1999, shares of [Qualcomm](https://en.wikipedia.org/wiki/Qualcomm "Qualcomm") rose in value by 2,619%, 12 other large-cap stocks each rose over 1,000% in value, and seven additional large-cap stocks each rose over 900% in value. Even though the Nasdaq Composite rose 85.6% and the [S&P 500](https://en.wikipedia.org/wiki/S%26P_500 "S&P 500") rose 19.5% in 1999, more stocks fell in value than rose in value as investors sold stocks in slower growing companies to invest in Internet stocks.[\[19\]](#cite_note-19)

An unprecedented amount of personal investing occurred during the boom and stories of people quitting their jobs to trade on the financial market were common.[\[20\]](#cite_note-20) The [news media](https://en.wikipedia.org/wiki/News_media "News media") took advantage of the public's desire to invest in the stock market; an article in _[The Wall Street Journal](https://en.wikipedia.org/wiki/The_Wall_Street_Journal "The Wall Street Journal")_ suggested that investors "re-think" the "quaint idea" of profits,[\[21\]](#cite_note-21) and [CNBC](https://en.wikipedia.org/wiki/CNBC "CNBC") reported on the stock market with the same level of suspense as many networks provided to the [broadcasting of sports events](https://en.wikipedia.org/wiki/Broadcasting_of_sports_events "Broadcasting of sports events").[\[16\]](#cite_note-enigma-16)[\[22\]](#cite_note-22)

At the height of the boom, it was possible for a promising dot-com company to become a [public company](https://en.wikipedia.org/wiki/Public_company "Public company") via an IPO and raise a substantial amount of money even if it had never made a profit—or, in some cases, realized any material revenue. People who received [employee stock options](https://en.wikipedia.org/wiki/Employee_stock_option "Employee stock option") became instant paper millionaires when their companies executed IPOs; however, most employees were barred from selling shares immediately due to [lock-up periods](https://en.wikipedia.org/wiki/Lock-up_period "Lock-up period").[\[18\]](#cite_note-swindle-18)\[_[page needed](https://en.wikipedia.org/wiki/Wikipedia:Citing_sources "Wikipedia:Citing sources")_\] The most successful entrepreneurs, such as [Mark Cuban](https://en.wikipedia.org/wiki/Mark_Cuban "Mark Cuban"), sold their shares or entered into [hedges](https://en.wikipedia.org/wiki/Hedge_\(finance\) "Hedge (finance)") to protect their gains. [Sir John Templeton](https://en.wikipedia.org/wiki/Sir_John_Templeton "Sir John Templeton") successfully [shorted](https://en.wikipedia.org/wiki/Short_\(finance\) "Short (finance)") many dot-com stocks at the peak of the bubble during what he called "temporary insanity" and a "once-in-a-lifetime opportunity". He shorted stocks just before the expiration of lockup periods ending six months after initial public offerings, correctly anticipating many dot-com company executives would sell shares as soon as possible, and that large-scale selling would force down share prices.[\[23\]](#cite_note-23)[\[24\]](#cite_note-24)

### Spending tendencies of dot-com companies\[[edit](https://en.wikipedia.org/w/index.php?title=Dot-com_bubble&action=edit§ion=5 "Edit section: Spending tendencies of dot-com companies")\]

[](https://en.wikipedia.org/wiki/File:Modo_Promo_CD.png)

[](https://en.wikipedia.org/wiki/File:Pets.com_sockpuppet.jpg)

dot-com companies spent most of their investments in marketing efforts. Left: A promotional music CD for the [Modo](https://en.wikipedia.org/wiki/Modo_\(wireless_device\) "Modo (wireless device)") pager, Right: The [Pets.com](https://en.wikipedia.org/wiki/Pets.com "Pets.com") sock puppet

Most dot-com companies incurred [net operating losses](https://en.wikipedia.org/wiki/Net_operating_loss "Net operating loss") as they spent heavily on advertising and promotions to harness [network effects](https://en.wikipedia.org/wiki/Network_effect "Network effect") to build [market share](https://en.wikipedia.org/wiki/Market_share "Market share") or [mind share](https://en.wikipedia.org/wiki/Mind_share "Mind share") as fast as possible, using the mottos "get big fast" and "get large or get lost". These companies offered their services or products for free or at a discount with the expectation that they could build enough [brand awareness](https://en.wikipedia.org/wiki/Brand_awareness "Brand awareness") to charge profitable rates for their services in the future.[\[25\]](#cite_note-lessons-25)[\[26\]](#cite_note-26)

The "growth over profits" mentality and the aura of "[new economy](https://en.wikipedia.org/wiki/New_economy "New economy")" invincibility led some companies to engage in lavish spending on elaborate business facilities and luxury vacations for employees. Upon the launch of a new product or website, a company would organize an expensive event called a [dot-com party](https://en.wikipedia.org/wiki/Dot-com_party "Dot-com party").[\[27\]](#cite_note-27)[\[28\]](#cite_note-28)

### Bubble in telecom\[[edit](https://en.wikipedia.org/w/index.php?title=Dot-com_bubble&action=edit§ion=6 "Edit section: Bubble in telecom")\]

In the five years after the American [Telecommunications Act of 1996](https://en.wikipedia.org/wiki/Telecommunications_Act_of_1996 "Telecommunications Act of 1996") went into effect, [telecommunications equipment](https://en.wikipedia.org/wiki/Telecommunications_equipment "Telecommunications equipment") companies invested more than $500 billion, mostly financed with debt, into laying fiber optic cable, adding new switches, and building wireless networks.[\[17\]](#cite_note-now-17) In many areas, such as the [Dulles Technology Corridor](https://en.wikipedia.org/wiki/Dulles_Technology_Corridor "Dulles Technology Corridor") in Virginia, governments funded technology infrastructure and created favorable business and tax law to encourage companies to expand.[\[29\]](#cite_note-29) The growth in capacity vastly outstripped the growth in demand.[\[17\]](#cite_note-now-17) [Spectrum auctions](https://en.wikipedia.org/wiki/Spectrum_auction "Spectrum auction") for [3G](https://en.wikipedia.org/wiki/3G "3G") in the United Kingdom in April 2000, led by [Chancellor of the Exchequer](https://en.wikipedia.org/wiki/Chancellor_of_the_Exchequer "Chancellor of the Exchequer") [Gordon Brown](https://en.wikipedia.org/wiki/Gordon_Brown "Gordon Brown"), raised £22.5 billion.[\[30\]](#cite_note-30) In Germany, in August 2000, the auctions raised £30 billion.[\[31\]](#cite_note-31)[\[32\]](#cite_note-32) A 3G [spectrum auction](https://en.wikipedia.org/wiki/Spectrum_auction "Spectrum auction") in the United States in 1999 had to be re-run when the winners defaulted on their bids of $4 billion. The re-auction netted 10% of the original sales prices.[\[33\]](#cite_note-33)[\[34\]](#cite_note-34) When financing became hard to find as the bubble burst, the high [debt ratios](https://en.wikipedia.org/wiki/Debt_ratio "Debt ratio") of these companies led to [bankruptcy](https://en.wikipedia.org/wiki/Bankruptcy "Bankruptcy").[\[35\]](#cite_note-35) Bond investors recovered just over 20% of their investments.[\[36\]](#cite_note-36) However, several telecom executives sold stock before the crash including [Philip Anschutz](https://en.wikipedia.org/wiki/Philip_Anschutz "Philip Anschutz"), who reaped $1.9 billion, [Joseph Nacchio](https://en.wikipedia.org/wiki/Joseph_Nacchio "Joseph Nacchio"), who reaped $248 million, and [Gary Winnick](https://en.wikipedia.org/wiki/Gary_Winnick "Gary Winnick"), who sold $748 million worth of shares.[\[37\]](#cite_note-37)

Bursting the bubble\[[edit](https://en.wikipedia.org/w/index.php?title=Dot-com_bubble&action=edit§ion=7 "Edit section: Bursting the bubble")\]

--------------------------------------------------------------------------------------------------------------------------------------------------

[](https://en.wikipedia.org/wiki/File:U.S._Treasuries.svg)

Historical government interest rates in the United States

Nearing the turn of the 2000s, spending on technology was volatile as companies prepared for the [Year 2000 problem](https://en.wikipedia.org/wiki/Year_2000_problem "Year 2000 problem"). There were concerns that computer systems would have trouble changing their clock and calendar systems from 1999 to 2000 which might trigger wider social or economic problems, but there was virtually no impact or disruption due to adequate preparation.[\[38\]](#cite_note-38) Spending on marketing also reached new heights for the sector: Two dot-com companies purchased ad spots for [Super Bowl XXXIII](https://en.wikipedia.org/wiki/Super_Bowl_XXXIII "Super Bowl XXXIII"), and 17 dot-com companies bought ad spots the following year for [Super Bowl XXXIV](https://en.wikipedia.org/wiki/Super_Bowl_XXXIV "Super Bowl XXXIV").[\[39\]](#cite_note-39)

On January 10, 2000, [America Online](https://en.wikipedia.org/wiki/America_Online "America Online"), led by [Steve Case](https://en.wikipedia.org/wiki/Steve_Case "Steve Case") and [Ted Leonsis](https://en.wikipedia.org/wiki/Ted_Leonsis "Ted Leonsis"), announced a [merger](https://en.wikipedia.org/wiki/Mergers_and_acquisitions "Mergers and acquisitions") with [Time Warner](https://en.wikipedia.org/wiki/Time_Warner "Time Warner"), led by [Gerald M. Levin](https://en.wikipedia.org/wiki/Gerald_M._Levin "Gerald M. Levin"). The merger was the largest to date and was questioned by many analysts.[\[40\]](#cite_note-40) Then, on January 30, 2000, 12 ads of the 61 ads for [Super Bowl XXXIV](https://en.wikipedia.org/wiki/Super_Bowl_XXXIV "Super Bowl XXXIV") were purchased by dot-coms (sources state ranges from 12 up to 19 companies depending on the definition of _dot-com company_). At that time, the cost for a 30-second commercial was between $1.9 million and $2.2 million.[\[41\]](#cite_note-41)[\[42\]](#cite_note-42)

Meanwhile, [Alan Greenspan](https://en.wikipedia.org/wiki/Alan_Greenspan "Alan Greenspan"), then [Chair of the Federal Reserve](https://en.wikipedia.org/wiki/Chair_of_the_Federal_Reserve "Chair of the Federal Reserve"), raised interest rates several times; these actions were believed by many to have caused the bursting of the dot-com bubble. According to [Paul Krugman](https://en.wikipedia.org/wiki/Paul_Krugman "Paul Krugman"), however, "he didn't raise interest rates to curb the market's enthusiasm; he didn't even seek to impose margin requirements on stock market investors. Instead, \[it is alleged\] he waited until the bubble burst, as it did in 2000, then tried to clean up the mess afterward".[\[43\]](#cite_note-43) Finance author and commentator [E. Ray Canterbery](https://en.wikipedia.org/w/index.php?title=E._Ray_Canterbery&action=edit&redlink=1 "E. Ray Canterbery (page does not exist)") agreed with Krugman's criticism.[\[44\]](#cite_note-44)

On Friday March 10, 2000, the NASDAQ Composite stock market index peaked at 5,048.62.[\[45\]](#cite_note-45) However, on March 13, 2000, news that [Japan](https://en.wikipedia.org/wiki/Economy_of_Japan "Economy of Japan") had once again entered a [recession](https://en.wikipedia.org/wiki/Lost_Decades "Lost Decades") triggered a global sell off that disproportionately affected technology stocks.[\[46\]](#cite_note-46) Soon after, [Yahoo!](https://en.wikipedia.org/wiki/Yahoo! "Yahoo!") and [eBay](https://en.wikipedia.org/wiki/EBay "EBay") ended merger talks and the Nasdaq fell 2.6%, but the [S&P 500](https://en.wikipedia.org/wiki/S%26P_500 "S&P 500") rose 2.4% as investors shifted from strong performing technology stocks to poor performing established stocks.[\[47\]](#cite_note-47)

On March 20, 2000, _[Barron's](https://en.wikipedia.org/wiki/Barron%27s_\(newspaper\) "Barron's (newspaper)")_ featured a cover article titled "Burning Up; Warning: Internet companies are running out of cash—fast", which predicted the imminent bankruptcy of many Internet companies.[\[48\]](#cite_note-48) This led many people to rethink their investments. That same day, [MicroStrategy](https://en.wikipedia.org/wiki/MicroStrategy "MicroStrategy") announced a revenue restatement due to aggressive accounting practices. Its stock price, which had risen from $7 per share to as high as $333 per share in a year, fell $140 per share, or 62%, in a day.[\[49\]](#cite_note-micro-49) The next day, the Federal Reserve raised interest rates, leading to an [inverted yield curve](https://en.wikipedia.org/wiki/Inverted_yield_curve "Inverted yield curve"), although stocks rallied temporarily.[\[50\]](#cite_note-50)

Tangentially to all of speculation, Judge [Thomas Penfield Jackson](https://en.wikipedia.org/wiki/Thomas_Penfield_Jackson "Thomas Penfield Jackson") issued his conclusions of law in the case of [_United States v. Microsoft Corp._ (2001)](https://en.wikipedia.org/wiki/United_States_v._Microsoft_Corp._\(2001\) "United States v. Microsoft Corp. (2001)") and ruled that Microsoft was guilty of [monopolization](https://en.wikipedia.org/wiki/Monopolization "Monopolization") and [tying](https://en.wikipedia.org/wiki/Tying_\(commerce\) "Tying (commerce)") in violation of the [Sherman Antitrust Act](https://en.wikipedia.org/wiki/Sherman_Antitrust_Act "Sherman Antitrust Act"). This led to a one-day 15% decline in the value of shares in Microsoft and a 350-point, or 8%, drop in the value of the Nasdaq. Many people saw the legal actions as bad for technology in general.[\[51\]](#cite_note-51) That same day, [Bloomberg News](https://en.wikipedia.org/wiki/Bloomberg_News "Bloomberg News") published a widely read article that stated: "It's time, at last, to pay attention to the numbers".[\[52\]](#cite_note-52)

On Friday, April 14, 2000, the Nasdaq Composite index fell 9%, ending a week in which it fell 25%. Investors were forced to sell stocks ahead of [Tax Day](https://en.wikipedia.org/wiki/Tax_Day_\(United_States\) "Tax Day (United States)"), the due date to pay taxes on gains realized in the previous year.[\[53\]](#cite_note-53) By June 2000, dot-com companies were forced to reevaluate their spending on advertising campaigns.[\[54\]](#cite_note-54) On November 9, 2000, [Pets.com](https://en.wikipedia.org/wiki/Pets.com "Pets.com"), a much-hyped company that had backing from Amazon.com, went out of business only nine months after completing its IPO.[\[55\]](#cite_note-pets-55)[\[56\]](#cite_note-56) By that time, most Internet stocks had declined in value by 75% from their highs, wiping out $1.755 trillion in value.[\[57\]](#cite_note-57) In January 2001, just three dot-com companies bought advertising spots during [Super Bowl XXXV](https://en.wikipedia.org/wiki/Super_Bowl_XXXV "Super Bowl XXXV").[\[58\]](#cite_note-58) The [September 11 attacks](https://en.wikipedia.org/wiki/September_11_attacks "September 11 attacks") accelerated the stock-market drop.[\[59\]](#cite_note-59) Investor confidence was further eroded by several [accounting scandals](https://en.wikipedia.org/wiki/Accounting_scandal "Accounting scandal") and the resulting bankruptcies, including the [Enron scandal](https://en.wikipedia.org/wiki/Enron_scandal "Enron scandal") in October 2001, the [WorldCom scandal](https://en.wikipedia.org/wiki/WorldCom_scandal "WorldCom scandal") in June 2002,[\[60\]](#cite_note-60) and the [Adelphia Communications Corporation](https://en.wikipedia.org/wiki/Adelphia_Communications_Corporation "Adelphia Communications Corporation") scandal in July 2002.[\[61\]](#cite_note-61)

By the end of the [stock market downturn of 2002](https://en.wikipedia.org/wiki/Stock_market_downturn_of_2002 "Stock market downturn of 2002"), stocks had lost $5 trillion in [market capitalization](https://en.wikipedia.org/wiki/Market_capitalization "Market capitalization") since the peak.[\[62\]](#cite_note-62) At its trough on October 9, 2002, the NASDAQ-100 had dropped to 1,114, down 78% from its peak.[\[63\]](#cite_note-63)[\[64\]](#cite_note-64)

Aftermath\[[edit](https://en.wikipedia.org/w/index.php?title=Dot-com_bubble&action=edit§ion=8 "Edit section: Aftermath")\]

------------------------------------------------------------------------------------------------------------------------------

After venture capital was no longer available, the operational mentality of executives and investors completely changed. A dot-com company's lifespan was measured by its [burn rate](https://en.wikipedia.org/wiki/Burn_rate "Burn rate"), the rate at which it spent its existing capital. Many dot-com companies ran out of capital and went through [liquidation](https://en.wikipedia.org/wiki/Liquidation "Liquidation"). Supporting industries, such as advertising and shipping, scaled back their operations as demand for services fell. However, many companies were able to endure the crash; 48% of dot-com companies survived through 2004, albeit at lower valuations.[\[25\]](#cite_note-lessons-25)

Several companies and their executives, including [Bernard Ebbers](https://en.wikipedia.org/wiki/Bernard_Ebbers "Bernard Ebbers"), [Jeffrey Skilling](https://en.wikipedia.org/wiki/Jeffrey_Skilling "Jeffrey Skilling"), and [Kenneth Lay](https://en.wikipedia.org/wiki/Kenneth_Lay "Kenneth Lay"), were accused or convicted of [fraud](https://en.wikipedia.org/wiki/Fraud "Fraud") for misusing shareholders' money, and the [U.S. Securities and Exchange Commission](https://en.wikipedia.org/wiki/U.S._Securities_and_Exchange_Commission "U.S. Securities and Exchange Commission") levied large fines against investment firms including [Citigroup](https://en.wikipedia.org/wiki/Citigroup "Citigroup") and [Merrill Lynch](https://en.wikipedia.org/wiki/Merrill_Lynch "Merrill Lynch") for misleading investors.[\[65\]](#cite_note-65)

After suffering losses, retail investors transitioned their investment portfolios to more cautious positions.[\[66\]](#cite_note-66) Popular [Internet forums](https://en.wikipedia.org/wiki/Internet_forum "Internet forum") that focused on [high tech](https://en.wikipedia.org/wiki/High_tech "High tech") stocks, such as [Silicon Investor](https://en.wikipedia.org/wiki/Silicon_Investor "Silicon Investor"), [Yahoo! Finance](https://en.wikipedia.org/wiki/Yahoo!_Finance "Yahoo! Finance"), and [The Motley Fool](https://en.wikipedia.org/wiki/The_Motley_Fool "The Motley Fool") declined in use significantly.[\[67\]](#cite_note-67)

### Job market and office equipment glut\[[edit](https://en.wikipedia.org/w/index.php?title=Dot-com_bubble&action=edit§ion=9 "Edit section: Job market and office equipment glut")\]

Layoffs of [programmers](https://en.wikipedia.org/wiki/Programmer "Programmer") resulted in a [general glut](https://en.wikipedia.org/wiki/General_glut "General glut") in the job market. University enrollment for computer-related degrees dropped noticeably.[\[68\]](#cite_note-68)[\[69\]](#cite_note-69) [Aeron chairs](https://en.wikipedia.org/wiki/Aeron_chair "Aeron chair"), which retailed for $1,100 each, were liquidated en masse.[\[70\]](#cite_note-70)

### Legacy\[[edit](https://en.wikipedia.org/w/index.php?title=Dot-com_bubble&action=edit§ion=10 "Edit section: Legacy")\]

As growth in the technology sector stabilized, companies consolidated; some, such as [Amazon.com](https://en.wikipedia.org/wiki/Amazon.com "Amazon.com"), [eBay](https://en.wikipedia.org/wiki/EBay "EBay"), [Nvidia](https://en.wikipedia.org/wiki/Nvidia "Nvidia") and [Google](https://en.wikipedia.org/wiki/Google "Google") gained market share and came to dominate their respective fields. The most valuable public companies are now generally in the technology sector.

In a 2015 book, venture capitalist [Fred Wilson](https://en.wikipedia.org/wiki/Fred_Wilson_\(financier\) "Fred Wilson (financier)"), who funded many dot-com companies and lost 90% of his net worth when the bubble burst, said about the dot-com bubble:

> A friend of mine has a great line. He says "Nothing important has ever been built without [irrational exuberance](https://en.wikipedia.org/wiki/Irrational_exuberance "Irrational exuberance")." Meaning that you need some of this mania to cause investors to open up their pocketbooks and finance the building of the railroads or the automobile or aerospace industry or whatever. And in this case, much of the capital invested was lost, but also much of it was invested in a very high [throughput](https://en.wikipedia.org/wiki/Throughput "Throughput") backbone for the Internet, and lots of software that works, and databases and server structure. All that stuff has allowed what we have today, which has changed all our lives... that's what all this speculative mania built.[\[71\]](#cite_note-71)

See also\[[edit](https://en.wikipedia.org/w/index.php?title=Dot-com_bubble&action=edit§ion=11 "Edit section: See also")\]

-----------------------------------------------------------------------------------------------------------------------------

* [Stock market crash](https://en.wikipedia.org/wiki/Stock_market_crash "Stock market crash")

* [Stock market crashes in India](https://en.wikipedia.org/wiki/Stock_market_crashes_in_India "Stock market crashes in India")

* [List of stock market crashes and bear markets](https://en.wikipedia.org/wiki/List_of_stock_market_crashes_and_bear_markets "List of stock market crashes and bear markets")

References\[[edit](https://en.wikipedia.org/w/index.php?title=Dot-com_bubble&action=edit§ion=12 "Edit section: References")\]

---------------------------------------------------------------------------------------------------------------------------------

1. **[^](#cite_ref-1 "Jump up")** ["The greatest defunct Web sites and dotcom disasters"](https://www.cnet.com/news/the-greatest-defunct-web-sites-and-dotcom-disasters/). _[CNET](https://en.wikipedia.org/wiki/CNET "CNET")_. June 5, 2008. [Archived](https://web.archive.org/web/20190828223335/https://www.cnet.com/news/the-greatest-defunct-web-sites-and-dotcom-disasters/) from the original on August 28, 2019. Retrieved February 10, 2020.

2. ^ [Jump up to: _**a**_](#cite_ref-valuation_2-0) [_**b**_](#cite_ref-valuation_2-1) Kumar, Rajesh (December 5, 2015). _Valuation: Theories and Concepts_. [Elsevier](https://en.wikipedia.org/wiki/Elsevier "Elsevier"). p. 25.

3. **[^](#cite_ref-3 "Jump up")** Powell, Jamie (2021-03-08). ["Investors should not dismiss Cisco's dot com collapse as a historical anomaly"](https://www.ft.com/content/81a03045-86f7-4e57-afbd-5ff83679615f). _[Financial Times](https://en.wikipedia.org/wiki/Financial_Times "Financial Times")_. [Archived](https://ghostarchive.org/archive/20221210/https://www.ft.com/content/81a03045-86f7-4e57-afbd-5ff83679615f) from the original on 2022-12-10. Retrieved 2022-04-06.

4. **[^](#cite_ref-4 "Jump up")** Edwards, Jim (December 6, 2016). ["One of the kings of the '90s dot-com bubble now faces 20 years in prison"](https://www.businessinsider.com/where-are-the-kings-of-the-1990s-dot-com-bubble-bust-2016-12). _[Business Insider](https://en.wikipedia.org/wiki/Business_Insider "Business Insider")_. [Archived](https://web.archive.org/web/20181011053734/https://www.businessinsider.com/where-are-the-kings-of-the-1990s-dot-com-bubble-bust-2016-12) from the original on October 11, 2018. Retrieved October 11, 2018.

5. **[^](#cite_ref-5 "Jump up")** A revealing look at the dot-com bubble of 2000 — and how it shapes our lives today | (ted.com)

6. ^ [Jump up to: _**a**_](#cite_ref-auto1_6-0) [_**b**_](#cite_ref-auto1_6-1) ‘Wallets and eyeballs’: how eBay turned the internet into a marketplace | eBay | The Guardian

7. ^ [Jump up to: _**a**_](#cite_ref-auto_7-0) [_**b**_](#cite_ref-auto_7-1) How Amazon Survived the Dot-Com Bubble | HBS Online

8. **[^](#cite_ref-8 "Jump up")** The new dot com bubble is here: it’s called online advertising – The Correspondent

9. **[^](#cite_ref-9 "Jump up")** Where Are They Now: 17 Dot-Com Bubble Companies And Their Founders (cbinsights.com)

10. **[^](#cite_ref-10 "Jump up")** The Dotcom Bubble Burst (2000) (internationalbanker.com)

11. **[^](#cite_ref-11 "Jump up")** ["Nasdaq peak of 5,048.62"](http://bigcharts.marketwatch.com/historical/default.asp?detect=1&symbol=NASDAQ&close_date=3%2F10%2F00&x=34&y=12). [Archived](https://web.archive.org/web/20171111145523/http://bigcharts.marketwatch.com/historical/default.asp?detect=1&symbol=NASDAQ&close_date=3%2F10%2F00&x=34&y=12) from the original on 2017-11-11. Retrieved 2022-04-15.

12. **[^](#cite_ref-12 "Jump up")** Kline, Greg (April 20, 2003). ["Mosaic started Web rush, Internet boom"](https://www.news-gazette.com/news/mosaic-started-web-rush-internet-boom/article_a459cd7f-dafe-5de4-a5fe-c3723a009af2.html). _[The News-Gazette](https://en.wikipedia.org/wiki/The_News-Gazette_\(Champaign-Urbana\) "The News-Gazette (Champaign-Urbana)")_. [Archived](https://web.archive.org/web/20200613132107/https://www.news-gazette.com/news/mosaic-started-web-rush-internet-boom/article_a459cd7f-dafe-5de4-a5fe-c3723a009af2.html) from the original on June 13, 2020. Retrieved February 10, 2020.

13. **[^](#cite_ref-13 "Jump up")** ["Issues in labor Statistics"](https://www.bls.gov/opub/btn/archive/computer-ownership-up-sharply-in-the-1990s.pdf) (PDF). [U.S. Department of Labor](https://en.wikipedia.org/wiki/U.S._Department_of_Labor "U.S. Department of Labor"). 1999. [Archived](https://web.archive.org/web/20170512120401/https://www.bls.gov/opub/btn/archive/computer-ownership-up-sharply-in-the-1990s.pdf) (PDF) from the original on 2017-05-12. Retrieved 2017-04-14.

14. **[^](#cite_ref-14 "Jump up")** Weinberger, Matt (February 3, 2016). ["If you're too young to remember the insanity of the dot-com bubble, check out these pictures"](https://www.businessinsider.com/history-of-the-dot-com-bubble-in-photos-2016-2/). _[Business Insider](https://en.wikipedia.org/wiki/Business_Insider "Business Insider")_. [Archived](https://web.archive.org/web/20200313233345/https://www.businessinsider.com/history-of-the-dot-com-bubble-in-photos-2016-2) from the original on March 13, 2020. Retrieved February 10, 2020.

15. **[^](#cite_ref-15 "Jump up")** ["Here's Why The Dot Com Bubble Began And Why It Popped"](https://www.businessinsider.com/heres-why-the-dot-com-bubble-began-and-why-it-popped-2010-12). _[Business Insider](https://en.wikipedia.org/wiki/Business_Insider "Business Insider")_. December 15, 2010. [Archived](https://web.archive.org/web/20200406151705/https://www.businessinsider.com/heres-why-the-dot-com-bubble-began-and-why-it-popped-2010-12) from the original on April 6, 2020. Retrieved February 10, 2020.

16. ^ [Jump up to: _**a**_](#cite_ref-enigma_16-0) [_**b**_](#cite_ref-enigma_16-1) [_**c**_](#cite_ref-enigma_16-2) [_**d**_](#cite_ref-enigma_16-3) Teeter, Preston; Sandberg, Jorgen (2017). "Cracking the enigma of asset bubbles with narratives". _Strategic Organization_. **15** (1): 91–99. [doi](https://en.wikipedia.org/wiki/Doi_\(identifier\) "Doi (identifier)"):[10.1177/1476127016629880](https://doi.org/10.1177%2F1476127016629880). [S2CID](https://en.wikipedia.org/wiki/S2CID_\(identifier\) "S2CID (identifier)") [156163200](https://api.semanticscholar.org/CorpusID:156163200).

17. ^ [Jump up to: _**a**_](#cite_ref-now_17-0) [_**b**_](#cite_ref-now_17-1) [_**c**_](#cite_ref-now_17-2) Litan, Robert E. (December 1, 2002). ["The Telecommunications Crash: What To Do Now?"](https://www.brookings.edu/research/the-telecommunications-crash-what-to-do-now/). _[Brookings Institution](https://en.wikipedia.org/wiki/Brookings_Institution "Brookings Institution")_. [Archived](https://web.archive.org/web/20180330212743/https://www.brookings.edu/research/the-telecommunications-crash-what-to-do-now/) from the original on March 30, 2018. Retrieved March 30, 2018.

18. ^ [Jump up to: _**a**_](#cite_ref-swindle_18-0) [_**b**_](#cite_ref-swindle_18-1) [Smith, Andrew](https://en.wikipedia.org/wiki/Andrew_Smith_\(author\) "Andrew Smith (author)") (2012). [_Totally Wired: On the Trail of the Great Dotcom Swindle_](https://books.google.com/books?id=GoDuPQAACAAJ). [Bloomsbury Books](https://en.wikipedia.org/wiki/Bloomsbury_Books "Bloomsbury Books"). [ISBN](https://en.wikipedia.org/wiki/ISBN_\(identifier\) "ISBN (identifier)") [978-1-84737-449-3](https://en.wikipedia.org/wiki/Special:BookSources/978-1-84737-449-3 "Special:BookSources/978-1-84737-449-3"). [Archived](https://web.archive.org/web/20200801023652/https://books.google.com/books/about/Totally_Wired.html?id=GoDuPQAACAAJ) from the original on 2020-08-01. Retrieved 2017-05-08.

19. **[^](#cite_ref-19 "Jump up")** [Norris, Floyd](https://en.wikipedia.org/wiki/Floyd_Norris "Floyd Norris") (January 3, 2000). ["THE YEAR IN THE MARKETS; 1999: Extraordinary Winners and More Losers"](https://www.nytimes.com/2000/01/03/business/the-year-in-the-markets-1999-extraordinary-winners-and-more-losers.html). _[The New York Times](https://en.wikipedia.org/wiki/The_New_York_Times "The New York Times")_. [Archived](https://web.archive.org/web/20170831061735/http://www.nytimes.com/2000/01/03/business/the-year-in-the-markets-1999-extraordinary-winners-and-more-losers.html) from the original on August 31, 2017. Retrieved August 26, 2017.

20. **[^](#cite_ref-20 "Jump up")** Kadlec, Daniel (August 9, 1999). ["Day Trading: It's a Brutal World"](http://content.time.com/time/magazine/article/0,9171,991726,00.html). _[Time](https://en.wikipedia.org/wiki/Time_\(magazine\) "Time (magazine)")_. [Archived](https://web.archive.org/web/20170415200633/http://content.time.com/time/magazine/article/0,9171,991726,00.html) from the original on April 15, 2017. Retrieved April 14, 2017.

21. **[^](#cite_ref-21 "Jump up")** Wysocki, Bernard (May 19, 1999). ["Companies Chose to Rethink A Quaint Concept: Profits"](https://www.wsj.com/articles/SB9270768713268007). _[The Wall Street Journal](https://en.wikipedia.org/wiki/The_Wall_Street_Journal "The Wall Street Journal")_. [Archived](https://web.archive.org/web/20210808220858/https://www.wsj.com/articles/SB9270768713268007) from the original on August 8, 2021. Retrieved August 8, 2021.

22. **[^](#cite_ref-22 "Jump up")** [Lowenstein, Roger](https://en.wikipedia.org/wiki/Roger_Lowenstein "Roger Lowenstein") (2004). [_Origins of the Crash: The Great Bubble and Its Undoing_](https://archive.org/details/originsofcrashgr00roge). [Penguin Books](https://en.wikipedia.org/wiki/Penguin_Books "Penguin Books"). p. [115](https://archive.org/details/originsofcrashgr00roge/page/115). [ISBN](https://en.wikipedia.org/wiki/ISBN_\(identifier\) "ISBN (identifier)") [978-1-59420-003-8](https://en.wikipedia.org/wiki/Special:BookSources/978-1-59420-003-8 "Special:BookSources/978-1-59420-003-8").

23. **[^](#cite_ref-23 "Jump up")** Langlois, Shawn (May 9, 2019). ["John Templeton profited from 'temporary insanity' in 2000 — now it's your turn, says longtime money manager"](https://www.marketwatch.com/story/john-templeton-profited-from-temporary-insanity-in-2000-now-its-your-turn-says-longtime-money-manager-2019-05-09). _[MarketWatch](https://en.wikipedia.org/wiki/MarketWatch "MarketWatch")_. [Archived](https://web.archive.org/web/20200731142657/https://www.marketwatch.com/story/john-templeton-profited-from-temporary-insanity-in-2000-now-its-your-turn-says-longtime-money-manager-2019-05-09) from the original on 2020-07-31. Retrieved 2021-04-03.

24. **[^](#cite_ref-24 "Jump up")** ["Old Dog, New Tricks"](https://www.forbes.com/forbes/2001/0528/054.html). _[Forbes](https://en.wikipedia.org/wiki/Forbes "Forbes")_. May 28, 2001. [Archived](https://web.archive.org/web/20210307040731/https://www.forbes.com/forbes/2001/0528/054.html) from the original on March 7, 2021. Retrieved April 3, 2021.

25. ^ [Jump up to: _**a**_](#cite_ref-lessons_25-0) [_**b**_](#cite_ref-lessons_25-1) BERLIN, LESLIE (November 21, 2008). ["Lessons of Survival, From the Dot-Com Attic"](https://www.nytimes.com/2008/11/23/business/23proto.html). _[The New York Times](https://en.wikipedia.org/wiki/The_New_York_Times "The New York Times")_. [Archived](https://web.archive.org/web/20170906100917/http://www.nytimes.com/2008/11/23/business/23proto.html) from the original on September 6, 2017. Retrieved August 26, 2017.

26. **[^](#cite_ref-26 "Jump up")** Dodge, John (May 16, 2000). ["MotherNature.com's CEO Defends Dot-Coms' Get-Big-Fast Strategy"](https://www.wsj.com/articles/SB958412442522904320). _[The Wall Street Journal](https://en.wikipedia.org/wiki/The_Wall_Street_Journal "The Wall Street Journal")_. [Archived](https://web.archive.org/web/20170415200406/https://www.wsj.com/articles/SB958412442522904320) from the original on April 15, 2017. Retrieved April 14, 2017.

27. **[^](#cite_ref-27 "Jump up")** Cave, Damien (April 25, 2000). ["Dot-com party madness"](https://www.salon.com/2000/04/25/party_5/). _[Salon](https://en.wikipedia.org/wiki/Salon_\(website\) "Salon (website)")_. [Archived](https://web.archive.org/web/20180309001604/https://www.salon.com/2000/04/25/party_5/) from the original on March 9, 2018. Retrieved March 8, 2018.

28. **[^](#cite_ref-28 "Jump up")** HuffStutter, P.J. (December 25, 2000). ["Dot-Com Parties Dry Up"](https://www.latimes.com/archives/la-xpm-2000-dec-25-mn-4559-story.html). _[Los Angeles Times](https://en.wikipedia.org/wiki/Los_Angeles_Times "Los Angeles Times")_. [Archived](https://web.archive.org/web/20200613132107/https://www.latimes.com/archives/la-xpm-2000-dec-25-mn-4559-story.html) from the original on June 13, 2020. Retrieved February 10, 2020.

29. **[^](#cite_ref-29 "Jump up")** Donnelly, Sally B.; Zagorin, Adam (August 14, 2000). ["D.C. Dotcom"](http://content.time.com/time/magazine/article/0,9171,52073-2,00.html). _[Time](https://en.wikipedia.org/wiki/Time_\(magazine\) "Time (magazine)")_. [Archived](https://web.archive.org/web/20200607165730/http://content.time.com/time/magazine/article/0,9171,52073-2,00.html) from the original on June 7, 2020. Retrieved February 10, 2020.

30. **[^](#cite_ref-30 "Jump up")** ["UK mobile phone auction nets billions"](http://news.bbc.co.uk/1/hi/business/727831.stm). _[BBC News](https://en.wikipedia.org/wiki/BBC_News "BBC News")_. April 27, 2000. [Archived](https://web.archive.org/web/20170823181352/http://news.bbc.co.uk/1/hi/business/727831.stm) from the original on August 23, 2017. Retrieved June 7, 2020.

31. **[^](#cite_ref-31 "Jump up")** Osborn, Andrew (November 17, 2000). ["Consumers pay the price in 3G auction"](https://www.theguardian.com/technology/2000/nov/17/citynews.business). _[The Guardian](https://en.wikipedia.org/wiki/The_Guardian "The Guardian")_. [Archived](https://web.archive.org/web/20200607165736/https://www.theguardian.com/technology/2000/nov/17/citynews.business) from the original on June 7, 2020. Retrieved June 7, 2020.

32. **[^](#cite_ref-32 "Jump up")** ["German phone auction ends"](https://money.cnn.com/2000/08/17/europe/german_umts/index.htm). _[CNN](https://en.wikipedia.org/wiki/CNN "CNN")_. August 17, 2000. [Archived](https://web.archive.org/web/20200607165726/https://money.cnn.com/2000/08/17/europe/german_umts/index.htm) from the original on June 7, 2020. Retrieved June 7, 2020.

33. **[^](#cite_ref-33 "Jump up")** Keegan, Victor (April 13, 2000). ["Dial-a-fortune"](https://www.theguardian.com/technology/2000/apr/13/mobilephones.victorkeegan). _[The Guardian](https://en.wikipedia.org/wiki/The_Guardian "The Guardian")_. [Archived](https://web.archive.org/web/20210205054229/https://www.theguardian.com/technology/2000/apr/13/mobilephones.victorkeegan) from the original on February 5, 2021. Retrieved June 7, 2020.

34. **[^](#cite_ref-34 "Jump up")** Sukumar, R. (April 11, 2012). ["Policy lessons from the 3G failure"](https://www.livemint.com/Opinion/FRQGcvIClZDzCS6EK0Cq4I/Views--Policy-lessons-from-the-3G-failure.html). _[Mint](https://en.wikipedia.org/wiki/Mint_\(newspaper\) "Mint (newspaper)")_. [Archived](https://web.archive.org/web/20200607165726/https://www.livemint.com/Opinion/FRQGcvIClZDzCS6EK0Cq4I/Views--Policy-lessons-from-the-3G-failure.html) from the original on June 7, 2020. Retrieved June 7, 2020.

35. **[^](#cite_ref-35 "Jump up")** White, Dominic (December 30, 2002). ["Telecoms crash 'like the South Sea Bubble'"](https://www.telegraph.co.uk/finance/2837764/Telecoms-crash-like-the-South-Sea-Bubble.html). _[The Daily Telegraph](https://en.wikipedia.org/wiki/The_Daily_Telegraph "The Daily Telegraph")_. [Archived](https://web.archive.org/web/20200607170853/https://www.telegraph.co.uk/finance/2837764/Telecoms-crash-like-the-South-Sea-Bubble.html) from the original on June 7, 2020. Retrieved June 7, 2020.

36. **[^](#cite_ref-36 "Jump up")** Hunn, David; Eaton, Collin (September 12, 2016). ["Oil bust on par with telecom crash of dot-com era"](https://www.houstonchronicle.com/business/energy/article/Oil-bust-on-par-wit-telecom-crash-of-dot-com-era-9218492.php). _[Houston Chronicle](https://en.wikipedia.org/wiki/Houston_Chronicle "Houston Chronicle")_. [Archived](https://web.archive.org/web/20200607165728/https://www.houstonchronicle.com/business/energy/article/Oil-bust-on-par-wit-telecom-crash-of-dot-com-era-9218492.php) from the original on June 7, 2020. Retrieved June 7, 2020.

37. **[^](#cite_ref-37 "Jump up")** ["Inside the Telecom Game"](https://www.bloomberg.com/news/articles/2002-08-04/inside-the-telecom-game). _[Bloomberg Businessweek](https://en.wikipedia.org/wiki/Bloomberg_Businessweek "Bloomberg Businessweek")_. August 5, 2002. [Archived](https://web.archive.org/web/20200607165728/https://www.bloomberg.com/news/articles/2002-08-04/inside-the-telecom-game) from the original on 2020-06-07. Retrieved 2020-06-07.

38. **[^](#cite_ref-38 "Jump up")** Marsha Walton; [Miles O'Brien](https://en.wikipedia.org/wiki/Miles_O%27Brien_\(journalist\) "Miles O'Brien (journalist)") (1 January 2000). ["Preparation pays off; world reports only tiny Y2K glitches"](https://web.archive.org/web/20041207152504/http://archives.cnn.com/2000/TECH/computing/01/01/y2k.weekend.wrap/index.html). _CNN_. Archived from [the original](http://archives.cnn.com/2000/TECH/computing/01/01/y2k.weekend.wrap/index.html) on 7 December 2004.

39. **[^](#cite_ref-39 "Jump up")** Beer, Jeff (2020-01-20). ["20 years ago, the dot-coms took over the Super Bowl"](https://www.fastcompany.com/90453258/20-years-ago-the-dot-coms-took-over-the-super-bowl). _Fast Company_. [Archived](https://web.archive.org/web/20200302153230/https://www.fastcompany.com/90453258/20-years-ago-the-dot-coms-took-over-the-super-bowl) from the original on 2020-03-02. Retrieved 2020-03-02.

40. **[^](#cite_ref-40 "Jump up")** Johnson, Tom (January 10, 2000). ["Thats AOL folks"](https://money.cnn.com/2000/01/10/deals/aol_warner/). _[CNN](https://en.wikipedia.org/wiki/CNN "CNN")_. [Archived](https://web.archive.org/web/20171211200333/http://money.cnn.com/2000/01/10/deals/aol_warner/) from the original on December 11, 2017. Retrieved October 29, 2018.

41. **[^](#cite_ref-41 "Jump up")** Pender, Kathleen (September 13, 2000). ["Dot-Com Super Bowl Advertisers Fumble / But Down Under, LifeMinders.com may win at Olympics"](https://www.sfgate.com/business/networth/article/Dot-Com-Super-Bowl-Advertisers-Fumble-But-Down-2739134.php). _[San Francisco Chronicle](https://en.wikipedia.org/wiki/San_Francisco_Chronicle "San Francisco Chronicle")_. [Archived](https://web.archive.org/web/20200302153229/https://www.sfgate.com/business/networth/article/Dot-Com-Super-Bowl-Advertisers-Fumble-But-Down-2739134.php) from the original on March 2, 2020. Retrieved March 2, 2020.

42. **[^](#cite_ref-42 "Jump up")** Kircher, Madison Malone (February 3, 2019). ["Revisiting the Ads From 2000's 'Dot-Com Super Bowl'"](https://nymag.com/intelligencer/2019/02/ads-2000-dot-com-super-bowl.html). _[New York](https://en.wikipedia.org/wiki/New_York_\(magazine\) "New York (magazine)")_. [Archived](https://web.archive.org/web/20200302153232/https://nymag.com/intelligencer/2019/02/ads-2000-dot-com-super-bowl.html) from the original on March 2, 2020. Retrieved March 2, 2020.

43. **[^](#cite_ref-43 "Jump up")** [Krugman, Paul](https://en.wikipedia.org/wiki/Paul_Krugman "Paul Krugman") (2009). [_The Return of Depression Economics and the Crisis of 2008_](https://archive.org/details/returnofdepressi00krug). W.W. Norton. p. [142](https://archive.org/details/returnofdepressi00krug/page/142). [ISBN](https://en.wikipedia.org/wiki/ISBN_\(identifier\) "ISBN (identifier)") [978-0-393-33780-8](https://en.wikipedia.org/wiki/Special:BookSources/978-0-393-33780-8 "Special:BookSources/978-0-393-33780-8").

44. **[^](#cite_ref-44 "Jump up")** Canterbery, E. Ray (2013). _The Global Great Recession_. World Scientific. pp. 123–135. [ISBN](https://en.wikipedia.org/wiki/ISBN_\(identifier\) "ISBN (identifier)") [978-981-4322-76-8](https://en.wikipedia.org/wiki/Special:BookSources/978-981-4322-76-8 "Special:BookSources/978-981-4322-76-8").

45. **[^](#cite_ref-45 "Jump up")** Long, Tony (March 10, 2010). ["March 10, 2000: Pop Goes the Nasdaq!"](https://www.wired.com/2010/03/0310nasdaq-bust/). _[Wired](https://en.wikipedia.org/wiki/Wired_\(magazine\) "Wired (magazine)")_. [Archived](https://web.archive.org/web/20180308234508/https://www.wired.com/2010/03/0310nasdaq-bust/) from the original on March 8, 2018. Retrieved March 8, 2018.

46. **[^](#cite_ref-46 "Jump up")** ["Nasdaq tumbles on Japan"](https://money.cnn.com/2000/03/13/markets/markets_newyork/). _[CNN](https://en.wikipedia.org/wiki/CNN "CNN")_. March 13, 2000. [Archived](https://web.archive.org/web/20181030035814/https://money.cnn.com/2000/03/13/markets/markets_newyork/) from the original on October 30, 2018. Retrieved October 29, 2018.

47. **[^](#cite_ref-47 "Jump up")** ["Dow wows Wall Street"](https://money.cnn.com/2000/03/15/markets/markets_newyork/). _[CNN](https://en.wikipedia.org/wiki/CNN "CNN")_. March 15, 2000. [Archived](https://web.archive.org/web/20181030111050/https://money.cnn.com/2000/03/15/markets/markets_newyork/) from the original on October 30, 2018. Retrieved October 29, 2018.

48. **[^](#cite_ref-48 "Jump up")** Willoughby, Jack (March 10, 2010). ["Burning Up; Warning: Internet companies are running out of cash—fast"](https://www.barrons.com/articles/SB953335580704470544). _[Barron's](https://en.wikipedia.org/wiki/Barron%27s_\(newspaper\) "Barron's (newspaper)")_. [Archived](https://web.archive.org/web/20180330001927/https://www.barrons.com/articles/SB953335580704470544) from the original on March 30, 2018. Retrieved March 30, 2018.

49. **[^](#cite_ref-micro_49-0 "Jump up")** ["MicroStrategy plummets"](https://money.cnn.com/2000/03/20/companies/microstrategy/). _[CNN](https://en.wikipedia.org/wiki/CNN "CNN")_. March 20, 2000. [Archived](https://web.archive.org/web/20181011172038/https://money.cnn.com/2000/03/20/companies/microstrategy/) from the original on October 11, 2018. Retrieved October 29, 2018.

50. **[^](#cite_ref-50 "Jump up")** ["Wall St.: What rate hike?"](https://money.cnn.com/2000/03/21/markets/markets_newyork/). _[CNN](https://en.wikipedia.org/wiki/CNN "CNN")_. March 21, 2000. [Archived](https://web.archive.org/web/20181011162024/https://money.cnn.com/2000/03/21/markets/markets_newyork/) from the original on October 11, 2018. Retrieved October 29, 2018.

51. **[^](#cite_ref-51 "Jump up")** ["Nasdaq sinks 350 points"](https://money.cnn.com/2000/04/03/markets/markets_newyork/). _[CNN](https://en.wikipedia.org/wiki/CNN "CNN")_. April 3, 2000. [Archived](https://web.archive.org/web/20180811164801/https://money.cnn.com/2000/04/03/markets/markets_newyork/) from the original on August 11, 2018. Retrieved October 29, 2018.

52. **[^](#cite_ref-52 "Jump up")** Yang, Catherine (April 3, 2000). ["Commentary: Earth To Dot Com Accountants"](https://www.bloomberg.com/news/articles/2000-04-02/commentary-earth-to-dot-com-accountants). _[Bloomberg News](https://en.wikipedia.org/wiki/Bloomberg_News "Bloomberg News")_. [Archived](https://web.archive.org/web/20170525120209/https://www.bloomberg.com/news/articles/2000-04-02/commentary-earth-to-dot-com-accountants) from the original on 2017-05-25. Retrieved 2017-05-04.

53. **[^](#cite_ref-53 "Jump up")** ["Bleak Friday on Wall Street"](https://money.cnn.com/2000/04/14/markets/markets_newyork/). _[CNN](https://en.wikipedia.org/wiki/CNN "CNN")_. April 14, 2000. [Archived](https://web.archive.org/web/20201127013703/https://money.cnn.com/2000/04/14/markets/markets_newyork/) from the original on November 27, 2020. Retrieved February 10, 2020.

54. **[^](#cite_ref-54 "Jump up")** Owens, Jennifer (June 19, 2000). ["IQ News: Dot-Coms Re-Evaluate Ad Spending Habits"](https://www.adweek.com/brand-marketing/iq-news-dot-coms-re-evaluate-ad-spending-habits-38208/). _[AdWeek](https://en.wikipedia.org/wiki/AdWeek "AdWeek")_. [Archived](https://web.archive.org/web/20170525091820/http://www.adweek.com/brand-marketing/iq-news-dot-coms-re-evaluate-ad-spending-habits-38208/) from the original on May 25, 2017.

55. **[^](#cite_ref-pets_55-0 "Jump up")** ["Pets.com at its tail end"](https://money.cnn.com/2000/11/07/technology/pets/). _[CNN](https://en.wikipedia.org/wiki/CNN "CNN")_. November 7, 2000. [Archived](https://web.archive.org/web/20180727024448/https://money.cnn.com/2000/11/07/technology/pets/) from the original on July 27, 2018. Retrieved October 29, 2018.

56. **[^](#cite_ref-56 "Jump up")** ["The Pets.com Phenomenon"](https://www.msnbc.com/msnbc-originals/watch/the-pets-com-phenomenon-789155395746). _[MSNBC](https://en.wikipedia.org/wiki/MSNBC "MSNBC")_. October 19, 2016. [Archived](https://web.archive.org/web/20180612135928/https://www.msnbc.com/msnbc-originals/watch/the-pets-com-phenomenon-789155395746) from the original on June 12, 2018. Retrieved June 28, 2018.

57. **[^](#cite_ref-57 "Jump up")** Kleinbard, David (November 9, 2000). ["The $1.7 trillion dot.com lesson"](https://money.cnn.com/2000/11/09/technology/overview/). _[CNN](https://en.wikipedia.org/wiki/CNN "CNN")_. [Archived](https://web.archive.org/web/20181024163116/https://money.cnn.com/2000/11/09/technology/overview/) from the original on October 24, 2018. Retrieved October 29, 2018.

58. **[^](#cite_ref-58 "Jump up")** Elliott, Stuart (January 8, 2001). ["In Super Commercial Bowl XXXV, the not-coms are beating the dot-coms"](https://www.nytimes.com/2001/01/08/business/media-business-advertising-super-commercial-bowl-xxxv-not-coms-are-beating-dot.html). _[The New York Times](https://en.wikipedia.org/wiki/The_New_York_Times "The New York Times")_. [Archived](https://web.archive.org/web/20170831223012/http://www.nytimes.com/2001/01/08/business/media-business-advertising-super-commercial-bowl-xxxv-not-coms-are-beating-dot.html) from the original on August 31, 2017. Retrieved August 26, 2017.

59. **[^](#cite_ref-59 "Jump up")** ["World markets shatter"](https://money.cnn.com/2001/09/11/europe/markets_europe/). _[CNN](https://en.wikipedia.org/wiki/CNN "CNN")_. September 11, 2001. [Archived](https://web.archive.org/web/20200920203418/https://money.cnn.com/2001/09/11/europe/markets_europe/) from the original on September 20, 2020. Retrieved February 10, 2020.

60. **[^](#cite_ref-60 "Jump up")** Beltran, Luisa (July 22, 2002). ["WorldCom files largest bankruptcy ever"](https://money.cnn.com/2002/07/19/news/worldcom_bankruptcy/). _[CNN](https://en.wikipedia.org/wiki/CNN "CNN")_. [Archived](https://web.archive.org/web/20181030111043/https://money.cnn.com/2002/07/19/news/worldcom_bankruptcy/) from the original on October 30, 2018. Retrieved October 29, 2018.

61. **[^](#cite_ref-61 "Jump up")** ["SEC Charges Adelphia and Rigas Family With Massive Financial Fraud"](https://www.sec.gov/news/press/2002-110.htm). _www.sec.gov_. [Archived](https://web.archive.org/web/20101109160208/http://www.sec.gov/news/press/2002-110.htm) from the original on 2010-11-09. Retrieved 2021-04-18.

62. **[^](#cite_ref-62 "Jump up")** Gaither, Chris; Chmielewski, Dawn C. (July 16, 2006). ["Fears of Dot-Com Crash, Version 2.0"](https://www.latimes.com/archives/la-xpm-2006-jul-16-fi-overheat16-story.html). _[Los Angeles Times](https://en.wikipedia.org/wiki/Los_Angeles_Times "Los Angeles Times")_. [Archived](https://web.archive.org/web/20191218173143/https://www.latimes.com/archives/la-xpm-2006-jul-16-fi-overheat16-story.html) from the original on December 18, 2019. Retrieved February 10, 2020.

63. **[^](#cite_ref-63 "Jump up")** Glassman, James K. (February 11, 2015). ["3 Lessons for Investors From the Tech Bubble"](https://www.nasdaq.com/articles/3-lessons-investors-tech-bubble-2015-02-11). _[Kiplinger's Personal Finance](https://en.wikipedia.org/wiki/Kiplinger%27s_Personal_Finance "Kiplinger's Personal Finance")_. [Archived](https://web.archive.org/web/20200404062028/https://www.nasdaq.com/articles/3-lessons-investors-tech-bubble-2015-02-11) from the original on 2020-04-04. Retrieved 2020-02-10.

64. **[^](#cite_ref-64 "Jump up")** Alden, Chris (March 10, 2005). ["Looking back on the crash"](https://www.theguardian.com/technology/2005/mar/10/newmedia.media). _[The Guardian](https://en.wikipedia.org/wiki/The_Guardian "The Guardian")_. [Archived](https://web.archive.org/web/20180104013428/https://www.theguardian.com/technology/2005/mar/10/newmedia.media) from the original on January 4, 2018. Retrieved March 30, 2018.

65. **[^](#cite_ref-65 "Jump up")** ["Ex-WorldCom CEO Ebbers found guilty on all counts – Mar. 15, 2005"](https://money.cnn.com/2005/03/15/news/newsmakers/ebbers/). _[CNN](https://en.wikipedia.org/wiki/CNN "CNN")_. [Archived](https://web.archive.org/web/20180703072335/http://money.cnn.com/2005/03/15/news/newsmakers/ebbers/) from the original on 2018-07-03. Retrieved 2021-06-20.

66. **[^](#cite_ref-66 "Jump up")** Reuteman, Rob (August 9, 2010). ["Hard Times Investing: For Some, Cash Is Everything And Only Thing"](https://www.cnbc.com/id/38308960). _[CNBC](https://en.wikipedia.org/wiki/CNBC "CNBC")_. [Archived](https://web.archive.org/web/20170525092042/http://www.cnbc.com/id/38308960) from the original on May 25, 2017. Retrieved September 9, 2017.

67. **[^](#cite_ref-67 "Jump up")** Forster, Stacy (January 31, 2001). ["Raging Bull Goes for a Bargain As Interest in Stock Chat Wanes"](https://www.wsj.com/articles/SB980897351252699393). _[The Wall Street Journal](https://en.wikipedia.org/wiki/The_Wall_Street_Journal "The Wall Street Journal")_. [Archived](https://web.archive.org/web/20181209213157/https://www.wsj.com/articles/SB980897351252699393) from the original on December 9, 2018. Retrieved December 9, 2018.

68. **[^](#cite_ref-68 "Jump up")** desJardins, Marie (October 22, 2015). ["The real reason U.S. students lag behind in computer science"](https://fortune.com/2015/10/22/u-s-students-computer-science/). _[Fortune](https://en.wikipedia.org/wiki/Fortune_\(magazine\) "Fortune (magazine)")_. [Archived](https://web.archive.org/web/20200307184124/https://fortune.com/2015/10/22/u-s-students-computer-science/) from the original on March 7, 2020. Retrieved February 10, 2020.

69. **[^](#cite_ref-69 "Jump up")** Mann, Amar; Nunes, Tony (2009). ["After the Dot-Com Bubble: Silicon Valley High-Tech Employment And Wages in 2001 and 2008"](https://www.bls.gov/opub/regional_reports/200908_silicon_valley_high_tech.htm). _[Bureau of Labor Statistics](https://en.wikipedia.org/wiki/Bureau_of_Labor_Statistics "Bureau of Labor Statistics")_. [Archived](https://web.archive.org/web/20181116080237/https://www.bls.gov/opub/regional_reports/200908_silicon_valley_high_tech.htm) from the original on 2018-11-16. Retrieved 2017-04-14.

70. **[^](#cite_ref-70 "Jump up")** Kennedy, Brian (September 15, 2006). ["Remembering the Dot-Com Throne"](https://nymag.com/news/intelligencer/21364/). _[New York](https://en.wikipedia.org/wiki/New_York_\(magazine\) "New York (magazine)")_. [Archived](https://web.archive.org/web/20200606014117/https://nymag.com/news/intelligencer/21364/) from the original on June 6, 2020. Retrieved February 10, 2020.

71. **[^](#cite_ref-71 "Jump up")** Donnelly, Jacob (February 14, 2016). ["Here's what the future of bitcoin looks like—and it's bright"](https://venturebeat.com/2016/02/14/heres-what-the-future-of-bitcoin-looks-like-and-its-bright/). _[VentureBeat](https://en.wikipedia.org/wiki/VentureBeat "VentureBeat")_. [Archived](https://web.archive.org/web/20170415200336/https://venturebeat.com/2016/02/14/heres-what-the-future-of-bitcoin-looks-like-and-its-bright/) from the original on April 15, 2017. Retrieved April 14, 2017.

Further reading\[[edit](https://en.wikipedia.org/w/index.php?title=Dot-com_bubble&action=edit§ion=13 "Edit section: Further reading")\]

-------------------------------------------------------------------------------------------------------------------------------------------

* Abramson, Bruce (2005). [_Digital Phoenix; Why the Information Economy Collapsed and How it Will Rise Again_](https://archive.org/details/digitalphoenixwh00abra). [MIT Press](https://en.wikipedia.org/wiki/MIT_Press "MIT Press"). [ISBN](https://en.wikipedia.org/wiki/ISBN_\(identifier\) "ISBN (identifier)") [978-0-262-51196-4](https://en.wikipedia.org/wiki/Special:BookSources/978-0-262-51196-4 "Special:BookSources/978-0-262-51196-4").

* Aharon, David Y.; Gavious, Ilanit; Yosef, Rami (2010). "Stock market bubble effects on mergers and acquisitions". _The Quarterly Review of Economics and Finance_. **50** (4): 456–70. [doi](https://en.wikipedia.org/wiki/Doi_\(identifier\) "Doi (identifier)"):[10.1016/j.qref.2010.05.002](https://doi.org/10.1016%2Fj.qref.2010.05.002).

* Cassidy, John (2009). [_Dot.con: How America Lost Its Mind and Its Money in the Internet Era_](https://books.google.com/books?id=jsuZnrzT6YsC). [HarperCollins](https://en.wikipedia.org/wiki/HarperCollins "HarperCollins"). [ISBN](https://en.wikipedia.org/wiki/ISBN_\(identifier\) "ISBN (identifier)") [9780061841781](https://en.wikipedia.org/wiki/Special:BookSources/9780061841781 "Special:BookSources/9780061841781").

* Cellan-Jones, Rory (2001). _Dot.Bomb: The Rise and Fall of Dot.com Britain_. Aurum. [ISBN](https://en.wikipedia.org/wiki/ISBN_\(identifier\) "ISBN (identifier)") [978-1854107909](https://en.wikipedia.org/wiki/Special:BookSources/978-1854107909 "Special:BookSources/978-1854107909").

* Daisey, Mike (2014). [_Twenty-one Dog Years: Doing Time at Amazon.com_](https://books.google.com/books?id=QhKhAgAAQBAJ). [Free Press](https://en.wikipedia.org/wiki/Free_Press_\(publisher\) "Free Press (publisher)"). [ISBN](https://en.wikipedia.org/wiki/ISBN_\(identifier\) "ISBN (identifier)") [978-0-7432-2580-9](https://en.wikipedia.org/wiki/Special:BookSources/978-0-7432-2580-9 "Special:BookSources/978-0-7432-2580-9").

* Goldfarb, Brent D.; Kirsch, David; Miller, David A. (April 24, 2006). "Was There Too Little Entry During the Dot Com Era?". _Robert H. Smith School Research Paper_ (RHS 06-029). [SSRN](https://en.wikipedia.org/wiki/SSRN_\(identifier\) "SSRN (identifier)") [899100](https://papers.ssrn.com/sol3/papers.cfm?abstract_id=899100).

* Kindleberger, Charles P. (2005). [_Manias, Panics, and Crashes: A History of Financial Crises_](https://books.google.com/books?id=nBb-xYi9O-sC). [John Wiley & Sons](https://en.wikipedia.org/wiki/John_Wiley_%26_Sons "John Wiley & Sons"). [ISBN](https://en.wikipedia.org/wiki/ISBN_\(identifier\) "ISBN (identifier)") [9780230365353](https://en.wikipedia.org/wiki/Special:BookSources/9780230365353 "Special:BookSources/9780230365353").\[_[permanent dead link](https://en.wikipedia.org/wiki/Wikipedia:Link_rot "Wikipedia:Link rot")_\]

* [Kuo, David](https://en.wikipedia.org/wiki/David_Kuo_\(author\) "David Kuo (author)") (2001). [_dot.bomb: My Days and Nights at an Internet Goliath_](https://books.google.com/books?id=SPeYMBXVFGoC). Little, Brown. [ISBN](https://en.wikipedia.org/wiki/ISBN_\(identifier\) "ISBN (identifier)") [978-0-316-60005-7](https://en.wikipedia.org/wiki/Special:BookSources/978-0-316-60005-7 "Special:BookSources/978-0-316-60005-7").

* [Lowenstein, Roger](https://en.wikipedia.org/wiki/Roger_Lowenstein "Roger Lowenstein") (2004). [_Origins of the Crash: The Great Bubble and Its Undoing_](https://archive.org/details/originsofcrashgr00roge). [Penguin Books](https://en.wikipedia.org/wiki/Penguin_Books "Penguin Books"). [ISBN](https://en.wikipedia.org/wiki/ISBN_\(identifier\) "ISBN (identifier)") [978-1-59420-003-8](https://en.wikipedia.org/wiki/Special:BookSources/978-1-59420-003-8 "Special:BookSources/978-1-59420-003-8").

* [Wolff, Michael](https://en.wikipedia.org/wiki/Michael_Wolff_\(journalist\) "Michael Wolff (journalist)") (1999). [_Burn Rate: How I Survived the Gold Rush Years on the Internet_](https://en.wikipedia.org/wiki/Burn_Rate_\(book\) "Burn Rate (book)"). [Orion Publishing Group](https://en.wikipedia.org/wiki/Orion_Publishing_Group "Orion Publishing Group"). [ISBN](https://en.wikipedia.org/wiki/ISBN_\(identifier\) "ISBN (identifier)") [9780752826066](https://en.wikipedia.org/wiki/Special:BookSources/9780752826066 "Special:BookSources/9780752826066"). _[Burn Rate](https://books.google.com/books?id=urRaPwAACAAJ)_ at [Google Books](https://en.wikipedia.org/wiki/Google_Books "Google Books").

Reader API

Get LLM-friendly input from a URL or a web search. Improve the factuality of your agent, RAG, GenAI system with a simple prefix.

Basic Usage

double_arrow

Read a URL

Add

https://r.jina.ai/ to any URL in your code or tool where LLM access is expected. This will return the main content of the page in clean, LLM-friendly text.search

Search a query

Add

https://s.jina.ai/ to your query. This will call the search engine and returns top-5 results with their URLs and contents, each in clean, LLM-friendly text.Advanced Usage

The behavior of the Reader API can be controlled with request headers. Here is a complete list of supported headers.

upload

Request

curl https://r.jina.ai/https://example.com

API Pricing

Our API pricing is structured around the quantity of tokens sent in the requests. For Reader API, it is the amount of tokens in the responses. This pricing model is applicable to all products in Jina AI's search foundation: Embedding, Reranking, Reader, Auto Fine-Tuning APIs. With the same API key, you have access to all API services.

Top up this API key by selecting the tokens you need

A tweet is about 20 tokens, a news article is about 1000 tokens, and Charles Dickens' novel "A Tale of Two Cities" has over a million tokens.

1M free tokens

Receive 1 million free tokens with each new API key, no credit card needed. Suitable for both personal and commercial projects.

Please input the right API key to top up

FAQ

At any time, press

/

to open search barReader-related common questions

What are the costs associated with using the Reader API?

How does the Reader API function?

Is the Reader API open source?

What is the typical latency for the Reader API?

Why should I use the Reader API instead of scraping the page myself?

Does the Reader API support multiple languages?

What should I do if a website blocks the Reader API?

Can the Reader API extract content from PDF files?

Can the Reader API process media content from web pages?

Is it possible to use the Reader API on local HTML files?

Does Reader API cache the content?

Can I use the Reader API to access content behind a login?

Can I use the Reader API to access PDF on arXiv?

How does image caption work in Reader?

What is the scalability of the Reader? Can I use it in production?

What is the rate limit of the Reader API?

API-related common questions

code

Can I use the same API key for embedding, reranking, reader, fine-tuning APIs?

code

Can I monitor the token usage of my API key?

code

What should I do if I forget my API key?

code

Do API keys expire?

code

Why is the first request for some models slow?

code

Is user input data used for training your models?

Billing-related common questions

attach_money

Is billing based on the number of sentences or requests?

attach_money

Is there a free trial available for new users?

attach_money

Are tokens charged for failed requests?

attach_money

What payment methods are accepted?

attach_money

Is invoicing available for token purchases?